Submitted by admin on Mon, 02/06/2017 - 11:22

Middle East the emerging new LNG player – as a consumer

The Middle East-North Africa (MENA) region is still the world’s premier LNG exporting area. But this is largely the creation of Qatar and Algeria. Increasing domestic demand and struggles on supply mean several countries in the region are turning to gas imports.

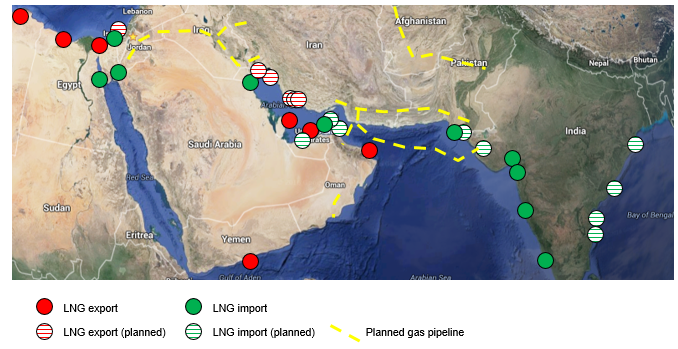

Iran has found it hard to progress its ambitious LNG goals, with the suspension of the NIOC, Persian and Pars LNG projects. Other established players are, for various reasons, unable to keep up with contracted supply, such as Oman, Yemen, Algeria and Egypt. And some countries are now considering shifting new gas supplies towards domestic use or importing gas themselves.

Oman’s 3-train, 10.4 Mtpa (million tonnes per year) nameplate LNG plant is under-utilized (72% utilisation rate in 2015) and would need tight gas (Khazzan-Makarem) to sustain its LNG exports. The Sultanate is now considering importing pipeline gas from Iran for re-export through the under-utilized LNG plant. In 2013, both countries signed an agreement, but international sanctions stalled it.

Now, the FEED (front-end engineering design) is already underway and the countries are planning to start the EPC (engineering, procurement and construction) work on the required subsea pipeline by 2017. This will take one year to complete. The pipeline will have the capacity to carry 1 Bcf/d (billion cubic feet per day) which may be raised to 1.5-2 Bcf/d as Oman’s domestic demand for power, petrochemicals and enhanced oil recovery continues to grow.

Yemen’s only LNG terminal has been shut-down since April 2015 due to domestic insecurity and war. The plant has a capacity of 6.7 Mtpa with three long-term sales contracts with GDF Suez SA, Korea Gas Corp. and Total SA and had a utilisation rate of only 21% in 2015.

Algeria increased LNG capacity in 2013 and 2014 with two new trains at Skikda and Arzew (together add 9.2 Mtpa of capacity), but is currently struggling to maintain exports due to fast growing domestic demand and a stagnant upstream sector. Total LNG installed capacity in Algeria is 27.2 Mtpa and LNG capacity utilisation rate was ~48% in 2014 (and 2015). The Skikda plant decommissioned two trains in early 2014 and will continue decommissioning ageing trains. Its gas production has been declining due to internal bureaucratic issues such as slow government approvals for projects and lack of investments. Algeria would need to step up its unconventional gas projects to maintain future exports.

From being an LNG exporter from 2005 until 2014, Egypt has transformed into an LNG importer. It imported around 76 shipments of LNG in 2015. Egypt currently has two regasification units (FSRU) under 5 year charters to EGAS (The Egyptian Natural Gas Holding Company): one from Hoegh LNG (Norway) which started up in April 2015 and the second from BW Gas (Singapore-based Norwegian group) which started up in October 2015. Egypt launched a tender in June 2016 for a third FSRU in 2017with a capacity of 750 MMcf/d (million cubic feet per day). The 2015 super-giant Zohr discovery will ease the need for future imports. The size of the field is estimated at 850 billion cubic metres (30 trillion cubic feet) and is expected to start production in Q4 2017. However, we still do not expect that Egypt will return to being a sizeable LNG exporter, unless it makes further large discoveries or, possibly, imports Cypriot or Israeli gas for liquefaction and re-export.

ADGAS, the LNG plant in Abu Dhabi, UAE, has a nameplate capacity of 5.6 Mtpa with Tokyo Electrical Power Company (TEPCO) as the main client. The contract for Japan LNG exports expires in 2019 and it is unclear if it will be renewed as the emirate is facing a possible gas crunch due to increasing domestic gas demand for power generation. Abu Dhabi is also exporting electricity to the northern emirates to meet their demand. Abu Dhabi received a FSRU from US firm Excelerate Energy at Ruwais with a capacity of 1 Mtpa (0.14 Bcf/d) and was installed amid delays to the construction of the Fujairah LNG import terminal. The emirate has already received its first cargo and is the first LNG import for Abu Dhabi which suggests that the emirate needs additional gas supplies before its planned onshore LNG import facility in Fujairah comes on stream.

Kuwait is already using a FSRU and is now planning an onshore LNG import terminal with 1.5 Bcf/d capacity. Bahrain is planning to develop a 0.8 Bcf/d LNG regasification terminal at a total cost of ~$900 mn and is expected to begin syndicating project finance. Jordan, with virtually no gas of its own, and badly affected by interruptions to Egyptian supplies, started LNG imports in 2015 through a contract with Shell of 0.49 Bcf/d capacity.

Even oil giant Saudi Arabia is considering gas imports, with Khalid Al-Falih, Minister of Energy, Industry and Mineral Resources of Saudi Arabia and chairman of Saudi Aramco, stating that Aramco was also considering investment in international gas.

The shifting global markets are affecting the world’s leading LNG player, Qatar. Doha is defending its Asian LNG markets against the rise of new competition from Australia and the US. Australia seems to be the bigger threat for now, as it has seven operating LNG developments and three more under construction. These are physically closer to Asian customers than the US plants, thus lowering shipping costs. Australia could be exporting 10 Bcf/d (~70 Mtpa) by 2020, almost equaling Qatar. Qatar has no plans for new LNG trains (which had a utilization capacity of 101% of nameplate in 2015) and new gas is more likely to go to rising domestic demand. To meet this, Qatar is prioritizing the Barzan project (North Field gas development) to increase production aimed for domestic use. It is expected to come online by this year. However, Qatar does have the ability to add ~10 Mtpa to LNG export capacity by debottlenecking.

Qatar, Saudi Arabia and Iran are expected to remain the largest gas producers in the Middle East through to 2030. Iran is likely to offer the most competitive gas supplies from the three large producers, but it is essential that it be able to maintain its gas exports to gain credibility in the region, which it could accomplish with its planned pipeline exports to Oman and its commitments of gas supply to a Baghdad power station and plans to increase exports to Iraq by 0.9 Bcf/d, to a total of 1.6 Bcf/d by 2017 to meet gas demand in Basra.

Iran is also considering pipeline exports to Kuwait (0.3 Bcf/d to 0.5 Bcf/d); and to the UAE (0.6 Bcf/d to 1.5 Bcf/d), but this will depend on successful political negotiations; however, it is relevant to note that routes for the Iran-Oman pipeline has been changed to avoid UAE waters. Qamar Energy forecasts that gas production in Iraq will reach 3.4 Bcf/d in 2020, but demand would be much higher at 5 Bcf/d; thus requiring increased imports to meet demand driven by the power sector. Iraq’s own LNG export plans appear, therefore, very much on the back burner.

Qamar sees The East Mediterranean having significant export potential (10+ Mtpa) depending on the chosen export route, politics and exploration results. The Key MENA Energy Scoreboard in our monthly newsletter tracks developments in the East Mediterranean gas sector.